UniFirst Corporation (NYSE:UNF) currently seems to be a smart choice for investors seeking exposure in the uniform-related space. It boasts solid growth prospects, evident from positive revision in its earnings estimates, and has strong fundamentals.

This Wilmington, MA-based company currently has a Zacks Rank #2 (Buy) and a VGM Score of B. It belongs to the Zacks Uniform and Related industry, which belongs to the broader Zacks Industrial Products sector.

The industry is currently placed in the top 5% (with Zacks Industry Rank #12) of more than 250 Zacks industries. Notably, the top 50% of the Zacks-ranked industries tend to outperform the bottom 50% by a factor of more than 2 to 1.

Below we discussed why it is worth investing in UniFirst.

Healthy Performance and Solid Growth Prospects: The company performed well in the past four quarters, surpassing estimates in all occasions. It has a positive earnings surprise of 25.60%, on average, for the last four quarters. Notably, its earnings of $2.52 per share surpassed the Zacks Consensus Estimate by 25.37% in the first quarter of fiscal 2020 (ended November 2019).

For fiscal 2020 (ending August 2020), the company anticipates earnings per share of $7.60-$7.92. This reflects revision from the previous projection of $7.47-$7.92.

Diversified Business: A solid customer base — including delivery service providers, wholesalers, service companies, automobile service centers, restaurants and others — are a boon for UniFirst. Based on service type, the company’s services can be segregated into three heads, comprising Core Laundry Operations, Specialty Garments and First Aid.

Also, its presence in multiple countries, including the United States, Europe and Canada, has strengthened its growth prospects.

For fiscal 2020, the company projects revenues of $1.860-$1.872 billion. Though the guidance reflects a slight revision from the previously mentioned $1.860-$1.880 billion (due to weakness in energy-related markets), it suggests growth from $1.809 billion generated in fiscal 2019 (ended August 2019).

The Zacks Consensus Estimate for UniFirst’s revenues is pegged at $1.87 billion for fiscal 2020 and $1.93 billion for fiscal 2021 (ending August 2021), suggesting year-over-year growth of 3.2% and 3.6%, respectively.

Acquired Assets: The company has been investing in acquisitions over time. In the first quarter of fiscal 2020, UniFirst used $39.3 million for acquisitions.

Notably, the company completed three buyouts (one of which was the industrial laundry business based in Missouri) in the fiscal first quarter.

Rewards to Shareholders: UniFirst is committed toward rewarding shareholders handsomely through dividend payments and share buybacks. In fiscal 2019 (ended August 2019), the company repurchased common stock worth $30.5 million and paid out dividends of $8.3 million. Further, it distributed dividends totaling $2.1 million and bought back shares worth $10 million in the first quarter of fiscal 2020.

It is worth mentioning here that the company announced an increase in its quarterly dividend rate from 11.25 cents to 25 cents in October 2019. We believe that healthy cash flow position will help the company in rewarding shareholders going forward.

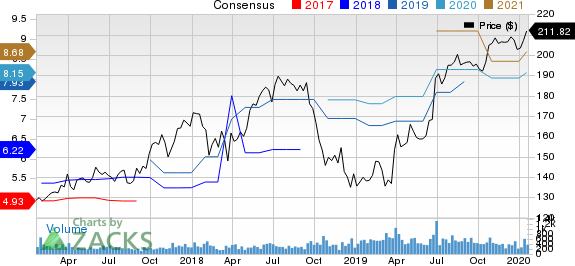

Share Price Performance & Earnings Estimates: We believe that impressive financial results helped drive sentiments for the stock. Notably, the company’s shares have gained 6.4% in the past three months compared with the industry’s growth of 5.1%.

Also, UniFirst’s earnings estimates have been revised positively in the past 30 days. Currently, the Zacks Consensus Estimate for its earnings is pegged at $8.16 for fiscal 2020 and $8.68 for fiscal 2021, reflecting growth of 1.7% and 2.8% from the respective 60-day-ago figures.

Unifirst Corporation Price and Consensus

Unifirst Corporation price-consensus-chart | Unifirst Corporation Quote

Other Key Picks

Some other top-ranked stocks in the sector are DXP Enterprises, Inc. (NASDAQ:DXPE) , Cintas Corporation (NASDAQ:CTAS) and Parker-Hannifin Corporation (NYSE:PH) . While DXP Enterprises currently sports a Zacks Rank #1 (Strong Buy), Cintas and Parker-Hannifin carry a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

In the past 60 days, earnings estimates for these stocks have improved for the current year. Further, positive earnings surprise for the last four quarters, on average, was 17.67% for DXP Enterprises, 8.50% for Cintas and 5.29% for Parker-Hannifin.

Biggest Tech Breakthrough in a Generation

Be among the early investors in the new type of device that experts say could impact society as much as the discovery of electricity. Current technology will soon be outdated and replaced by these new devices. In the process, it’s expected to create 22 million jobs and generate $12.3 trillion in activity.

A select few stocks could skyrocket the most as rollout accelerates for this new tech. Early investors could see gains similar to buying Microsoft (NASDAQ:MSFT) in the 1990s. Zacks’ just-released special report reveals 8 stocks to watch. The report is only available for a limited time.

See 8 breakthrough stocks now>>

Unifirst Corporation (UNF): Free Stock Analysis Report

Cintas Corporation (CTAS): Free Stock Analysis Report

Parker-Hannifin Corporation (PH): Free Stock Analysis Report

DXP Enterprises, Inc. (DXPE): Free Stock Analysis Report

Original post

Zacks Investment Research